Certain tanker sectors have ridden a series of exceptional events to net exceptional returns.

Pre-COVID19

Early 2018 was one of the most challenging periods seen in the tanker sector, as a combination of reduced cargo volumes and excess supply of tankers provided a sustained downward pressure on rates until 4Q 2018. From 4Q 2018, however, tanker rates improved as a result of seasonal factors, rising US exports and increased Chinese imports driven by the 35% fall in the price of crude oil during the period. Following the late 2018 short-lived rebound in tanker trades, accelerated net tonnage growth observed in 1H 2019 (particularly in the VLCC segment) and the OPEC-driven production cuts, this put downward pressure on freight earnings that remained subdued during that period.

Nonetheless, the 2019 tensions in the Middle East, and the widening of US sanctions (with charterers avoiding tankers that have been linked to trades with Venezuela and Iran) were seen as the main factors behind boosted demand in October-November 2019. In addition, the approaching implementation of the new International Maritime Organisation’s (IMO) low-sulphur fuel regulations (with underlining limited tonnage supply due to scrubber retrofitting, which particularly intensified among larger vessels in early 4Q 2019 - 2.3% of the total fleet underwent retrofitting in October 2019) attracted demand for tonnage.

In 2019, China maintained its spot as the top importer of crude, with imports standing at 9.1m bpd, up by 11% year-on-year. To put this into perspective, China accounted for more than 80% of global oil demand growth in 2019. China’s significant import demand in 2019 has been primarily driven by the start-up of two new refineries. However, this growth in 2019 has appeared insufficient to offset declining imports elsewhere, with the US turning from a net importer to a net exporter in 2019. Europe has also been a substantial crude oil importer over the years, with the continent’s demands marginally boosted to 10.4m bpd in 2019, up 1% year-on-year.

|

Tanker Size |

1Q 2019 |

2Q 2019 |

3Q 2019 |

4Q 2019 |

|

MR1 |

$ 15,436 |

$ 13,618 |

$ 12,349 |

$ 19,243 |

|

MR2 |

$ 15,839 |

$ 11,006 |

$ 11,325 |

$ 24,006 |

|

LR1 |

$ 16,011 |

$ 13,733 |

$ 13,435 |

$ 23,249 |

|

LR2 |

$ 20,471 |

$ 19,033 |

$ 17,890 |

$ 31,788 |

|

Aframax |

$ 24,085 |

$ 16,961 |

$ 15,911 |

$ 46,738 |

|

Suezmax |

$ 22,967 |

$ 18,652 |

$ 18,217 |

$ 59,994 |

|

VLCC |

$ 27,754 |

$ 20,169 |

$ 29,456 |

$ 81,394 |

Table 1: Daily rates of tankers per quarter 2019

Looking at market fundamentals in early 2020, these remained favourable to tanker owners with a positive reaction to the US-China "Phase One" trade deal. As part of the trade agreement signed in mid-January 2020, China agreed to import an additional USD 52bn of US energy goods by 2021. Moreover, in February 2020, China not only reduced its tariff on imports of US crude from 5% to 2.5%, but also announced that companies could apply for exemptions from tariffs on a wide range of US goods, including crude oil.

With regard to the supply of tonnage at year-end, crude oil fleet growth projected to stand at moderate levels of about 3% in 2020, when compared to over 4% in 2019. Moreover, scrubber retrofit time had been expected to continue to impact tanker supply, with more than 1.5% of the crude tanker fleet and 0.7% of the products tanker fleet expected to undertake retrofitting in 2020. Furthermore, availability of large crude carriers was expected to also be hit due to a number of VLCCs used for floating storage as a hedge against future prices. More specifically, the National Iranian Tanker Co.’s fleet including sanctioned units ranging from Aframaxes to VLCCs, was primarily engaged in floating storage off Iran. Tanker owner Euronav NV was among the first to take a position; as a part of the IMO 2020 sulphur emissions regulations and as part of the company's strategy, Euronav purchased 420,000 tonnes of compliant fuel oil which is currently stored in the two ULCCs.

The lifting of US sanctions on Cosco Shipping Tanker (Dalian) Co. in early 2020, and the return of its vessels to the market increased tonnage availability, contributing to a significant easing in tanker market conditions in January and early February 2020.

Early to mid-COVID19 period

By February 2020, the impact of COVID-19 on the crude oil market, and thus, the tanker rate environment, had become increasingly evident. Brent crude prices came under significant pressure, falling from an average of circa USD 64.40bbl to around USD 55bbl in February, as Chinese oil demand dropped severely. Oil demand was predominantly hampered by travel restrictions, business closures and disruptions, as well as reduced refinery run rates by Chinese refiners (such as Sinopec and PetroChina, as well as non-state owned refiners) and the build-up of products inventories, with a number of crude cargoes reportedly being diverted to other countries. Travel restrictions due to containment efforts limited the use of jet fuel, and supply chains slowed, with industrial activity declining as companies sent employees home (this has very direct effects on oil consumption and informs near-term calculations of real oil demand).

We have traced reports indicating that these disruptions have had additional spill-over effects on maritime operations for tankers (and of course, other vessel classes) calling at Chinese ports or being built or retrofitted with scrubbers at Chinese shipyards; with regard to latter, these areas have witnessed noteworthy delays. A Scandinavia-based tanker owner has indicated that in early February 2020, his company was informed by a Chinese yard that the redelivery of certain vessels that were being retrofitted with scrubbers (and were supposed to be back in the water by mid-to-late February), would be delayed by a “minimum of three weeks”; this came as certain yards reportedly issued force majeure certificated for a number of units. We note that in most cases, and according to certain shipping sources, under the legal protection of force majeure, companies can seek to avoid penalties that may arise from not fulfilling contracts. Nevertheless, this causes headaches for shippers who bet on the cost-benefit of scrubbers in contrast to utilising VLSFO. Furthermore, in early February, an executive at China State Shipbuilding Corp., (which employees more than 300,000 workers at various facilities), stated that “we are working at around a quarter of our capacity”, and that the “supply chain for some yards has been seriously impacted”, with spares not being delivered and engineers staying in self-isolation. In the wider context of things, while the Chinese New Year generally delays scheduled work by up to a month, COVID-19 is said to have added circa three weeks (or even more) in this equation.

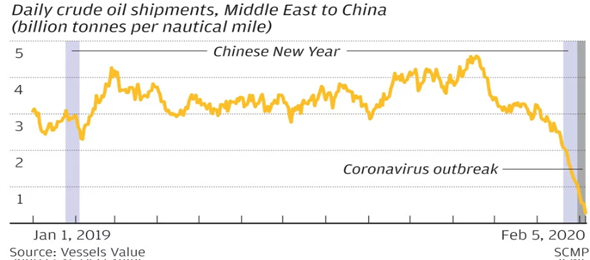

Port calls have also been affected, with port calls throughout vessel classes falling by an estimated 30% in February, according to shipping research sources; specifically, daily crude oil shipments from the Middle East to China plunged, as is evident in the following graph:

According to a data analytics firm, shipments of oil from the Middle East, China’s largest source of the commodity, were a mere 12% of the dwt-mile shipped on the same day (5 February) in 2019.

According to the International Energy Agency (IEA), global refining throughput in 2020 is expected to decline for a second consecutive year, falling below 2017 levels as demand for transport fuels plunges in the wake of COVID-19. The IEA also estimated that global oil demand would decline in 2020 for the first time since 2009, as COVID-19 continues to spread around the world, adding severe restraints on both travel and broader economic activity. Evidently, in the past few weeks, COVID-19 has developed from being a Chinese health crisis to a global pandemic and economic emergency.

With regard to wet trade, strong winter demand and rates for tankers at the end of 4Q 2019 were abruptly disrupted by the aforementioned factors, with average daily earnings for VLCCs dropping from circa USD 94,286 per day at the start of January, to around USD 23,036 per day. This decline was also driven by the higher cost of fuel caused by the implementation of the IMO 2020 sulphur cap, as average earnings are reported on a time charter equivalent (TCE) basis, which take fuel costs into account, and as these rose for non-scrubber fitted tankers, the overall average decline in tanker earnings was amplified. This downward spiral was further driven by the lifting of US sanctions against Cosco Shipping Tanker (Dalian), resulting in the re-entering of additional vessel capacity into the market, amplifying the supply gut and its effect on average market rates.

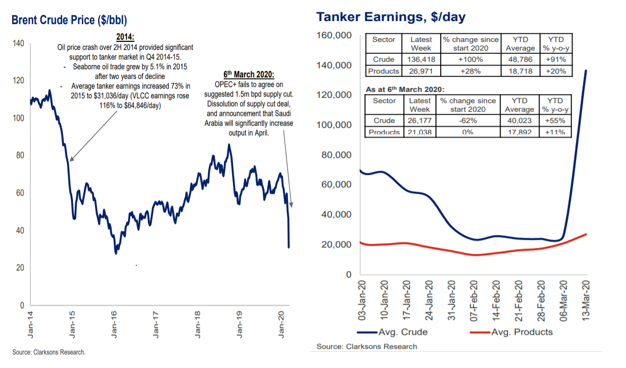

Responding to the distressed oil demand environment, in early March 2020, members of the Organisation of the Petroleum Exporting Countries (OPEC) and their international allies (together known as OPEC+), initiated discussions for the collective management of the slump triggered by the COVID-19 outbreak. However, these talks collapsed, revealing deep divisions over how to deal with recent developments. Saudi Arabia demanded that Russia contributes to a proposed reduction of a further 1.5m bpd, insisting that OPEC would not reduce supply without the support on non-members. Russia and Saudi Arabia failed to agree on this measure and the supply-cut deal abruptly dissolved, with Saudi Arabia announcing that it will significantly increase output in April 2020 (to a record of 12.3m bpd in April 2020), in an apparent attempt to “punish” Russia and squeeze the US shale industry. Other Gulf producers such as the United Arab Emirates (UAE) also joined the “battle” for market share.

According to an energy company executive, the breakdown resembles a “classic game theory outcome”, with each side standing to gain if the other side backs down (and both sides losing if none of them does). These developments drove a further downward spiral in crude oil prices, threatening global oil markets with additional supply amidst a new price war between top oil producers Saudi Arabia and Russia. The effects of these developments on crude oil prices, and their subsequent effects on demand and rates for crude oil and products tankers, are illustrated in the graphs below:

By 13 March 2020, the breakdown of the OPEC+ discussions and the potential surge in additional oil supply drove average VLCC rates from the mid-USD 20,000s per day to circa USD 279,000 per day, (daily rates for scrubber-fitted VLCCs from the Middle East to the US reached in excess of USD 440,000 in mid-March), with OPEC’s extra production potentially translating into demand for a further 60 VLCCs in the market. In addition to materially supporting the tanker market, the collapse in oil prices also reduced fuel costs (further supporting earnings capability), narrowing the spread between Very Low Sulphur Fuel Oil (VLSFO) and High Sulphur Fuel Oil (HSFO) in key ports (to around USD 100 – USD 150 per tonne). A reversal of this spread trend remains possible, although this is difficult to gauge given the volatility in global supply and demand.

Near-term Outlook

Global oil supply growth projections in 2020 have increased to circa 1.4%, with further output driven by Saudi Arabia, Russia and other OPEC members (partly offset by slower US shale output growth and falling output in Libya and Venezuela). The COVID-19 shock on Chinese oil demand, as well as significant increases in Middle Eastern production, led to oil prices falling to just over USD 25bbl by mid-March 2020 (witnessing their biggest daily rout since the 1991 Gulf War), reflecting a deterioration of around 40% from their mid-February level, with markets bracing for oil prices somewhere in the low USD 20s.

In addition to supporting crude tanker earnings, the drop in the price of crude leads to improved refinery margins and further potential for global inventory building, which is expected to assist in offsetting the negative impact of declining oil demand on seaborne wet trade. Potential use of tonnage as floating storage is also expected to absorb tanker supply, and in the medium term, it remains likely that tanker demand growth could be impacted by the slower growth in US production and long-haul crude exports.

These developments have shifted control of the market to the hands of tanker owners, which are determining whether to take advantage of surging spot rates or engage them in floating storage deals; the flip in the crude oil market’s forward curve to a “contango” (where forward prices are above spot prices), has been a key factor in driving demand for storage. Overall, the trading arms of oil majors as well as other prominent trading concerns appear willing to maintain the high demand for large crude carriers for the near-term as they have clearly exhibited their intentions to maintain floating storage units until crude prices have readjusted.

The short-term outlook for the oil and tankers market will ultimately depend on the success of respective governments to contain the impact/spread of the COVID-19 outbreak, leading to less uncertainty and a rebalancing of economic activity. According to recent shipping research and media sources, it has been suggested that it might be possible to bring the outbreak under control in China by the end of April, with the country’s facilities becoming more operational and potentially running at a higher capacity by May 2020, bringing China’s oil imports to more normal levels of over 9.1m bpd. In 1Q 2020, we believe that China would have suffered the most with a year-on-year drop in oil demand of over 1.5 m bpd as factories shut down and transportation has become restricted. In 2Q 2020, and as the situation in China improves, demand disruptions are expected to persist in some other large economies, such as Japan, and even more so in the US and Europe.

Although the extent and severity are yet to be determined, the outbreak is currently believed to be approaching its peak across many other regions including Asia, North America and Europe. Containment measures imposed in the aforementioned regions are expected to have a smaller impact on oil demand; however, the situation for significant importers of crude such as Italy (about 1.1m bpd) remains very troublesome. As we move through the second half of the year, demand and crude imports are estimated to improve, likely returning to levels closer to 2H 2019.

The surge in rates for crude oil carriers commencing in mid-March 2020 may likely be a short/medium-term effect, especially if provisional fixtures do not materialise in actual contracts. While fixture activity at high levels could continue for the largest part of 1H 2020, certain traders may soon find charter rates way beyond viability levels. A recent example of this has been reported with regard to the trading arm of the Chinese state-owned Sinopec, Unipec, which according to market sources, have recently attempted to cancel or defer the loading of at least four VLCCs from the Middle East in April due to higher freight rates. Unipec was reported to have allocated the cargoes as part of its long-term supply contracts, but the current rate environment is making the shipments considerably more expensive, while in tandem, Unipec’s parent is said to be planning to reduce crude processing at its refineries in May because of suppressed fuel demand in China, reducing the amount of crude it needs from Unipec.

Furthermore, based on current contango levels, a shipbroking source has assessed that to make floating storage viable a VLCC will require up to maximum of USD 72,000 per day for a three-month time charter. However, we have seen a rapidly rising market in mid-March 2020, meaning that at current rate levels, freight is too high to justify floating storage play. Potentially, there could be a time when storage rates and the contango converge. As mentioned, given that there are now signs that China’s economic activity is re-emerging, this may come just in time (from an oil demand perspective) as the Western Countries enter a lock-down.

Several operators may look to adjust their positions accordingly, but as mentioned, the power has for the time being shifted to the hands of tonnage-owning companies. According to tanker owners contacted, it is difficult to estimate when the large crude carriers market could peak, but after the initial upswing in refinery margins from the lower prices charged from Saudi crude oil, the upsurge in tanker spot rates have seen refinery margins return to normal levels. Even though it would not be possible to estimate the actual market correction levels and timing, our sources believe that spot market rates will gradually deteriorate, although still allowing for significant profitability for more crude carriers (with VLCCs in some cases earning as much as 10 times their net break-even levels or even higher, and the material surge in VLCC rates also having significant spill-over effects on smaller tanker sizes as larger crude carriers are being booked). We are already witnessing this correctional phase, which has seen average spot rates for crude carriers drop by circa 50% in late-March 2020 following their upward spiral during the first half of the month.

Furthermore, one must keep in mind that as China’s labour force gradually returns to work after an extended Lunar New Year holiday imposed by the government in an effort to contain the pandemic, shipyards are expected to be slowly ramping up their activities, with concerns about calling at Chinese ports (either due to fear of contraction or due to operational disturbance at ports) slowly being alleviated. With regard to yard delays, the managing director of Wah Kwong Maritime Transport Holdings, which has two ships under construction at Chinese shipyards, indicated that he foresees the overall delay to be one to two months post-February 2020, depending on the capability and resilience of different yards.

Insights from the stock markets

|

Year-to-Date (as at 23 March 2020) |

Month-to-Date (as at 23 March 2020) |

||

|

WTI Crude Oil (Nymex) |

-61.74% |

-47.81% |

|

|

Brent Crude (ICE) |

-59.05% |

-46.50% |

|

|

Baltic Exchange Dirty Tanker Index |

-24.59% |

27.99% |

|

|

DHT Holdings Inc. |

-28.99% |

5.95% |

|

|

Euronav N.V. |

-32.22% |

-8.90% |

|

|

Frontline Ltd |

-47.82% |

-18.07% |

|

|

International Seaways Inc. |

-37.20% |

-6.03% |

|

|

Nordic American Tanker Ltd |

-48.37% |

-21.12% |

|

|

Teekay Tankers Ltd |

-20.86% |

14.62% |

|

|

Tsakos Energy Navigation |

-52.98% |

-25.18% |

|

|

Ardmore Shipping Corp. |

-53.92% |

-24.18% |

|

|

Diamond S Shipping Inc. |

-41.52% |

-4.95% |

|

|

Scorpio Tankers Inc. |

-59.38% |

-19.21% |

In line with the upswing in tanker rates during mid-March 2020, the Baltic Exchange Dirty Tanker Index has improved substantially. While at the time this initially saw improvements in the prices of the common stocks of some major US-listed tanker shipping companies (listed above), such gains have also been reversed in most cases alongside the recent correction in tanker rates during late-March 2020.